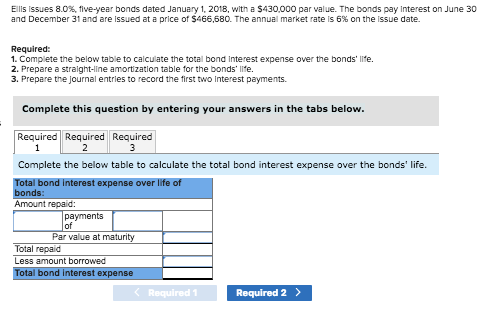

Solved Required Information Exercise 6-4B Calculate

Free, open source, cross-platform audio software for multi-track recording and editing

Dezembro 24, 2020Form 990 N filers must use a new sign-in process to file their annual reports

Junho 24, 2021Solved Required Information Exercise 6-4B Calculate

Content

And companies are required by law to state which accounting method they used in their published financials. Using LIFO, calculate ending inventory, cost of goods sold, sales revenue, and gross profit. Using FIFO, calculate ending inventory, cost of goods sold, sales revenue, and gross profit. During the year 2010, the inventory of D’s gift shop decreased by 50,000. If the income statement for the year 2010 reported costs of goods sold of 350,000, purchases during the year must have amounted to __________. What are the LIFO, FIFO, and Weighted Average inventory valuation methods?

Which inventory method most likely will result in the highest ending inventory when costs are rising?

Last-in, first-out, or LIFO, uses the most recent costs first. When prices are rising, you prefer LIFO because it gives you the highest cost of goods sold and the lowest taxable income.

This principle of consistency, using the same method period after period, enables companies to present the fairest numbers and pay the appropriate taxes based on their reported income. If they want to change their method, they must get approval from the Internal Revenue Service via IRS Form 3115 after the end of the tax year. The only requirement when choosing a method is that determine which method will result in higher profitability when inventory costs are rising. at the end of the period, the sum of COGS and ending inventory equals the cost of goods available. A different bead company in the area, Coastal Beads, Inc., calculated its inventory value at the end of a period using the gross profit method. From its accounting software, it reports the following figures. Companies generally report inventory value at their paid cost.

Rising Prices and FIFO

If the ending inventory is overstated, the cost of merchandise sold would be understated, gross profit overstated, and net income overstated. If the ending inventory is understated, the cost of merchandise sold would be overstated, gross profit understated, and net income understated. The controller uses the information in the above table and the FIFO inventory method formula to calculate the cost of goods sold for December and the inventory balance as of the end of December. This ensures that the oldest product or the older items are sold out maintaining the physical flow or the product flow making place for the newest stock. There are many accounting software available for the same.

When the textbook is sold, the bookstore removes the cost of $85 from its inventory and reports the $85 as the cost of goods sold on the income statement that reports the sale of the textbook. The trend above shows that the more recent inventory costs have increased versus earlier costs. Conversely, COGS would be lower under LIFO – i.e. the cheaper inventory costs were recognized – leading to higher net income. The importance of FIFO vs. LIFO is due to the fact that inventory cost recognition directly impacts a company’s current period net profits .

What Inventory Method Gives the Highest Income?

This means that if inventory values were to plummet, their valuations would represent the market value instead of LIFO, FIFO, or average cost. FIFO can be a better indicator of the value for ending inventory because the older items have been used up while the most recently acquired items reflect current market prices. The Last-In, First-Out method assumes that the last or moreunit to arrive in inventory is sold first. The older inventory, therefore, is left over at the end of the accounting period. The inventory profit is considered a holding gain caused by the increase in the acquisition price of the inventory between the time that the firm purchased and then sold the item. Some accountants argue that these profits are overstated because, in order to stay in business, a going concern must replace its inventory at current acquisition prices or replacement costs.

The Inventory account is normally adjusted only at the end of the year. During the year the Inventory account will show only the cost of inventory as of the end of the previous year. In this situation, the inventory purchased earlier is less expensive compared to recent purchases. This is unchanged each year since 1,200 units are said to remain in inventory. Finished inventory are items ready for sale that can be bought and delivered to consumers. The Last-In, First-Out method assumes that the last unit to arrive in inventory or more recent is sold first.

Dollar Value LIFO Method

The theory is based on the logic of selling those inventories which are first purchased. Therefore, companies issue materials and utilize the goods that are set at higher price first. In case your inventory costs are falling, FIFO might be the best option for you. The above equation shows that the inventory value affects the cost and thereby the gross profit. For example, if the closing stock is overvalued, it will inflate the current year’s profit and reduce profits for subsequent years. Inventory refers to the goods meant for sale or unsold goods.

- This method achieves the proper matching of sales revenue and cost of goods sold when the individual units in the inventory are unique.

- Income tax deferral is the most common answer for using LIFO while evaluating current assets.

- If you plan to apply for a loan, always choose the technique that provides the highest inventory value.

- Therefore the commodities at the end of inventory layers become old and gradually lose their value.

- Cost of goods sold is an important accounting term to familiarize yourself with.

First In, First Out is an accounting method in which assets purchased or acquired first are disposed of first. Accounting policies are the specific principles and procedures implemented by a company’s management that are used to prepare financial statements. Companies often use LIFO when attempting to reduce its tax liability. LIFO usually doesn’t match the physical movement of inventory, as companies may be more likely to try to move older inventory first. However, companies like car dealerships or gas/oil companies may try to sell items marked with the highest cost to reduce their taxable income.

Average Cost Method

This is a substantial figure, considering that Safeway’s net income for 2020 was $185.0 million. In an economy where prices are rising, LIFO results in the lowest gross margin and the lowest ending inventory. The figures in this table are taken from the example shown in the article entitled “Application of different cost flow assumptions.” The average cost fell between these two extremes for all three accounts.

- In some jurisdictions, all companies are required to use the FIFO method to account for inventory.

- Overvaluation or undervaluation can give a misleading picture of the working capital position and the overall financial position.

- The weighted average inventory costing method, also called the average cost inventory method, is one of the GAAP-compliant approaches companies use to value their business stock.

- This method is based on the premise that the first inventory purchased is the first to be sold.

- It’s important to keep shareholders happy, and the best way to do this is to give them a great return on their money investment by choosing the best inventory valuation method.

- Your choice can lead to drastic differences in the cost of goods sold, net income and ending inventory.